Navigating the world of cryptocurrency in India can feel like decoding a complex puzzle, especially with new rules rolling out. If you’ve been trading or thinking about it, the Budget 2026 updates are something you can’t ignore.

Here is a simple breakdown of how crypto is taxed today and what is changing from April 1, 2026.

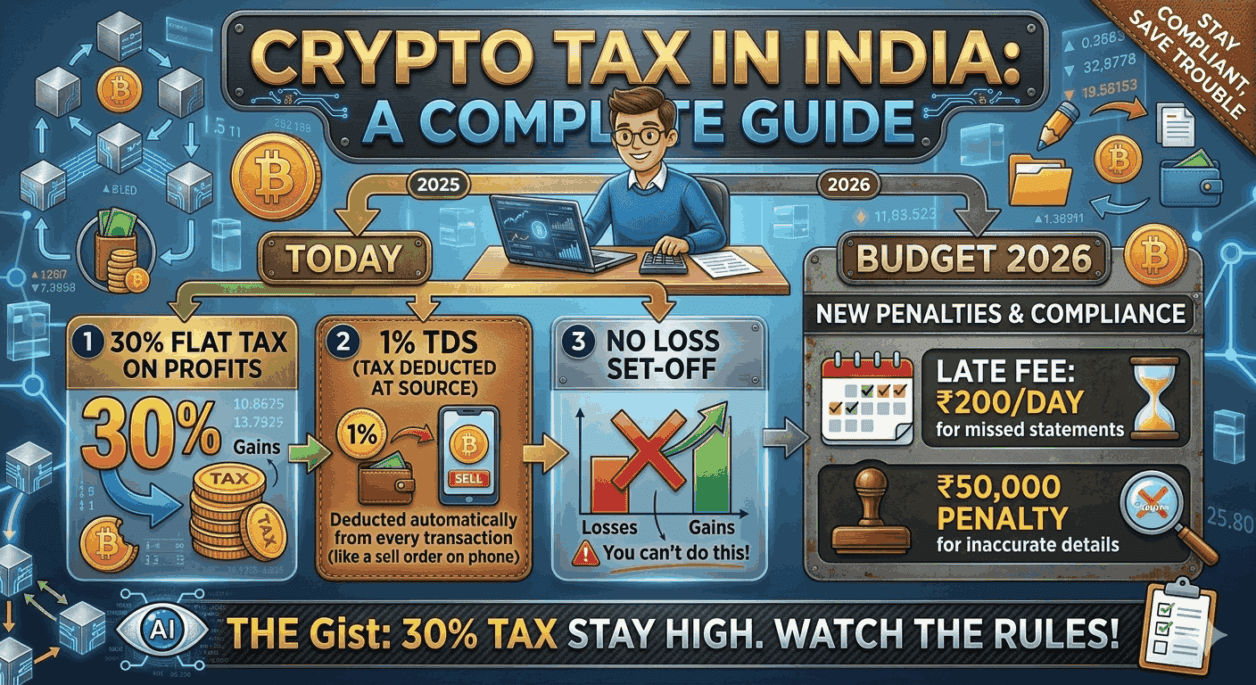

1. The “Big Three” Rules (Current Law)

The core tax structure for crypto (technically called Virtual Digital Assets or VDAs) remains the same as it has been since 2022. There are three main pillars:

30% Flat Tax on Profits: If you buy Bitcoin for ₹1 Lakh and sell it for ₹1.5 Lakh, you owe 30% tax on that ₹50,000 profit. It doesn’t matter if you held it for one day or three years; the rate stays the same.

1% TDS (Tax Deducted at Source):

Every time you sell or “transfer” crypto, 1% of the total transaction value is deducted. Think of this as a digital footprint that tells the government a transaction happened.

No “Loss Set-off”: This is the harshest part. If you make a profit of ₹10,000 on Ethereum but lose ₹10,000 on Dogecoin, you cannot cancel them out. You still have to pay 30% tax on the ₹10,000 profit, even though your net gain is zero.

2. What’s Changing After Budget 2026?

While the tax rates didn’t change, the penalties for staying silent did. The government is moving from “watching” to “enforcing.” Starting April 1, 2026, new compliance rules kick in under a new framework:

The “Late Fee” for Statements: If you (or the exchange you use) fail to submit the required transaction statements, there is now a penalty of ₹200 per day.

The “Mistake Penalty”: If you provide inaccurate information in your reports or fail to fix errors when flagged, you could face a flat penalty of ₹50,000.

Strict AI Monitoring: The tax department is using advanced AI to cross-check the 1% TDS data against what you declare in your ITR (Income Tax Return). If there’s a mismatch, a notice is likely to follow.

3. How to Stay Safe and Compliant

To avoid these new penalties and the high 30% tax “surprises,” keep these tips in mind:

Track Everything: Keep a log of every buy, sell, and swap. Even swapping one crypto for another is considered a “transfer” and is taxable.

Use Reputable Exchanges: Indian exchanges usually handle the 1% TDS for you automatically. If you use international exchanges, the responsibility to pay that 1% TDS often falls on you.

Report Honestly: With the new ₹50,000 penalty for “inaccurate particulars,” it is cheaper to pay the tax than to risk hiding the income.

The Bottom Line

The government’s message in Budget 2026 is clear: Tax rates are staying high, and the room for error is getting smaller. If you are a crypto investor in India, 2026 is the year to move from “casual trading” to “disciplined record-keeping.”

Disclaimer: This post is for educational purposes. Tax laws can be complex; always consult a qualified tax professional before filing your returns.