Whether you’re looking to protect your health, your car, or your family’s future, navigating the world of insurance can feel like decoding a foreign language. Here is a breakdown of the most common types of insurance plans and how they actually work.

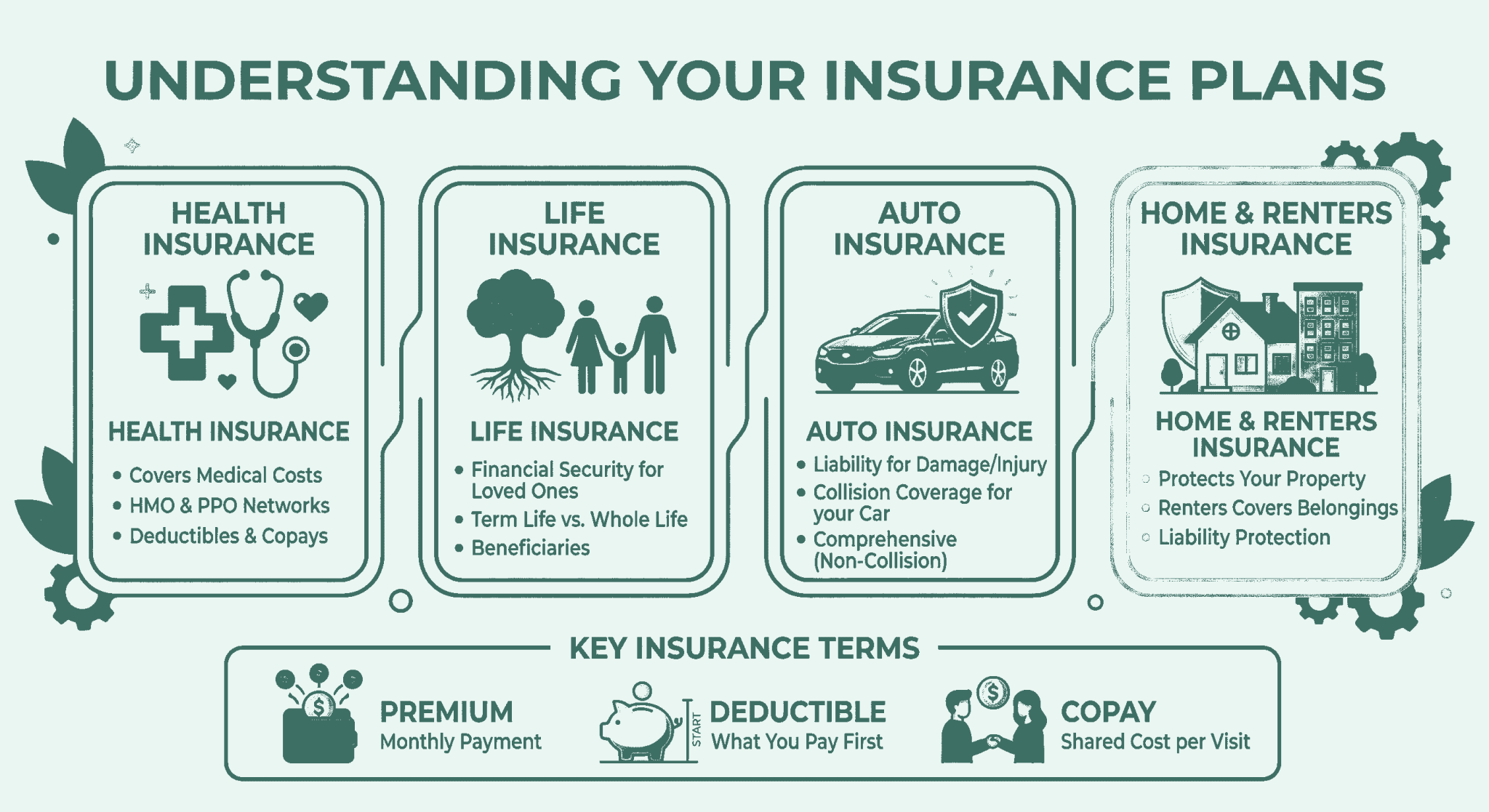

1. Health Insurance

Health insurance covers medical expenses, ranging from routine check-ups to major surgeries. The “type” of plan you choose determines which doctors you can see and how much you pay out-of-pocket.

HMO (Health Maintenance Organization): Usually requires you to see doctors within a specific network and get referrals from a primary care physician (PCP) to see specialists.

PPO (Preferred Provider Organization): Offers more flexibility. You can see specialists without a referral and use out-of-network doctors, though it costs more.

High-Deductible Health Plan (HDHP): Lower monthly premiums but higher costs when you actually seek care. These are often paired with a Health Savings Account (HSA).

2. Life Insurance

Life insurance provides a financial safety net for your beneficiaries (like a spouse or children) after you pass away.

Term Life: Covers you for a specific period (e.g., 10, 20, or 30 years). It is generally the most affordable option and is designed to provide protection during your peak “financial responsibility” years.

Whole Life (Permanent): Covers you for your entire life and includes a “cash value” component that grows over time. Premiums are significantly higher than term life.

3. Auto Insurance

Most places require basic auto insurance by law, but there are several layers of protection:

Liability: Covers damage you cause to others (their car or their medical bills).

Collision: Pays to repair your car after an accident, regardless of who is at fault.

Comprehensive: Covers non-collision events like theft, fire, or “acts of God” (e.g., a tree falling on your car).

4. Property Insurance

Whether you own or rent, protecting your living space is vital.

Homeowners Insurance: Covers the structure of your home and your personal belongings against perils like fire or windstorms. It also provides liability if someone is injured on your property.

Renters Insurance: Your landlord’s insurance only covers the building. Renters insurance is essential to protect your personal items (electronics, furniture, clothes) from theft or damage.

Key Insurance Terms to Know

To compare these plans effectively, you’ll need to understand these three “price tags”:

| Term | Definition |

| Premium | The fixed amount you pay (usually monthly) to keep the policy active. |

| Deductible | The amount you pay out-of-pocket before the insurance company starts chipping in. |

| Copay/Co-insurance | Your share of the costs for a specific service (e.g., a $30 flat fee for a doctor visit). |

Insurance isn’t about hoping for the worst; it’s about planning so that the worst doesn’t derail your financial future.