In the last few years, India’s digital lending space has exploded. While the convenience of getting money in “5 minutes” is tempting, a dark reality lurks behind many of these mobile applications. Predatory loan apps have led to financial ruin, social humiliation, and, tragically, a string of suicides across the country.

If you are looking for quick cash, reading this could save your life and your reputation.

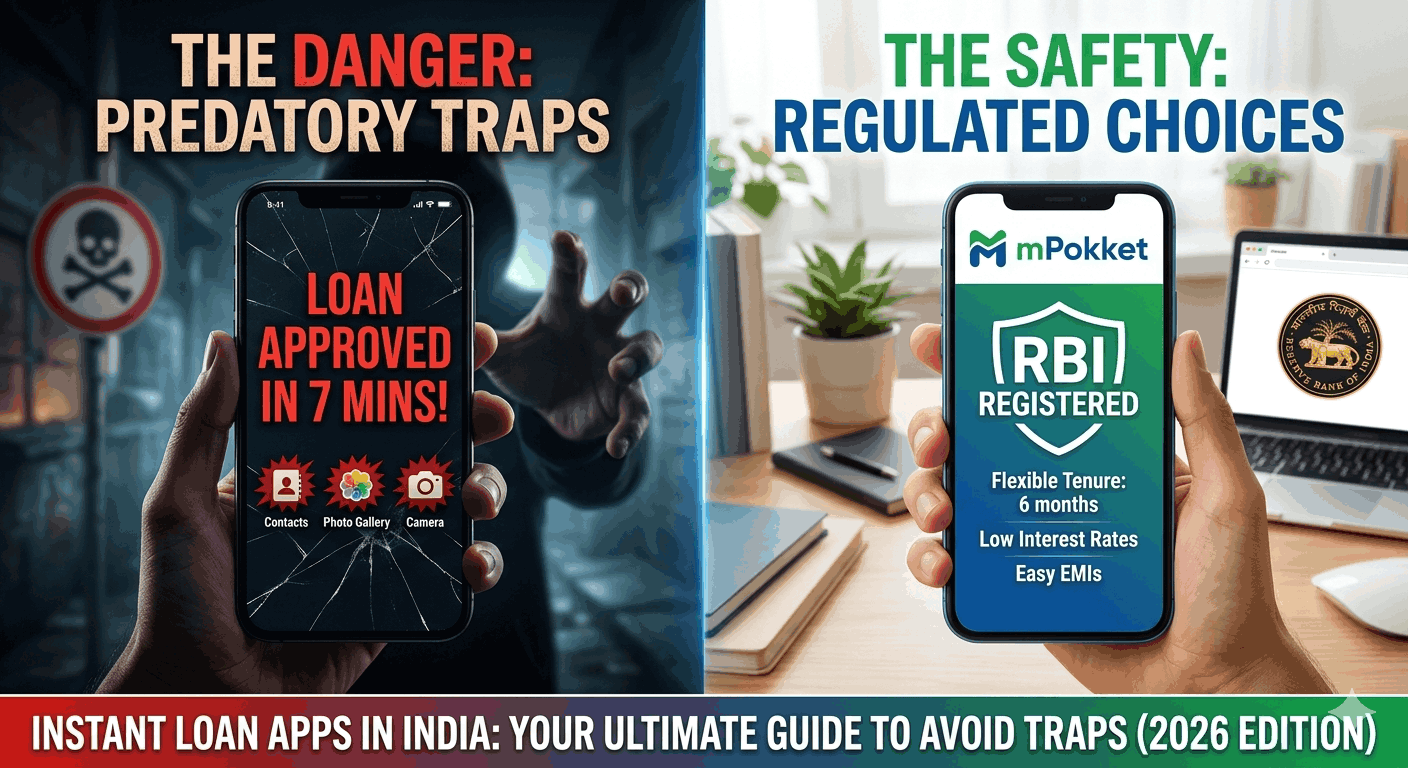

The “7-Day” Trap: How Predatory Apps Work

Illegal loan apps operate with a ruthless blueprint designed to pull you into a debt spiral. Unlike legitimate banks, they don’t care about your credit score; they care about your data.

1. Data as Collateral

When you install an unregulated app, it asks for permissions that no bank would ever need: access to your Contacts, Photo Gallery, and GPS. This is the “ammunition” they use to blackmail you if you miss a payment by even an hour.

2. The Debt Spiral

Most trap apps offer “Short-term” loans of 7 to 15 days with astronomical interest rates—often exceeding 300% APR. If you can’t pay, they “recommend” another app (which they also own) to pay off the first one. Within a month, a small ₹5,000 loan can balloon into a debt of lakhs.

he Human Cost: Real-Life Incidents of Harassment

The tactics used by these apps are not just unethical; they are criminal. Here are some documented types of harassment that have led to tragic ends:

Social Shaming: Agents call every person in your contact list—your boss, your parents, your neighbors—telling them you are a “fraudster.”

Morphing Images: In a horrific trend seen in 2024 and 2025, recovery agents have used AI to morph borrowers’ photos into obscene images, threatening to leak them to family groups unless “fines” are paid.

The Bhopal Tragedy (2023): An IT professional killed his wife and two children before taking his own life. His suicide note revealed he was trapped by multiple loan apps that were threatening to leak his private data.

The Andhra Pradesh Incident (2026): A college student committed suicide after a “loan bot” sent a broadcast message to all his college professors labeling him a criminal over a mere ₹3,000 default.

New RBI Guidelines (2025–2026): Your Shield

To combat this, the Reserve Bank of India introduced the Digital Lending Directions, 2025. Under these new laws:

Direct Disbursal: Money must move from the Bank/NBFC directly to the borrower—no third-party “wallets” allowed.

Cooling-off Period: Borrowers now have a mandatory window (at least 24 hours) to exit a loan penalty-free.

Data Sovereignty: Apps are strictly prohibited from accessing your Contacts and Media.

The “White List”: Since July 2025, the RBI maintains a central directory of authorized Digital Lending Apps (DLAs) on its official website.

Spotting the Difference: The mPokket Case Study

Not all apps are traps. There are genuine, regulated platforms that provide a safe experience. A well-known example in India is mPokket.

My Recommendation: Apps like mPokket are genuine because they follow the law. They offer comfortable installments and, while they do use “reminder robot calls” and add late penalties, they never violate your privacy or threaten your social circle.

Primary Keywords: Online loan app harassment India, RBI registered loan apps 2026, mPokket review, avoid loan traps, cybercrime loan app complaint.